Is a SPAC approach relevant for Swiss companies? (Part 2)

Some good and some bad news for potential targets

Following my initial article on SPACs, I was surprised to see how many people and Swiss companies that had been averse to the idea of going public for a long time had, all of a sudden, developed a keen interest in SPACs.

I just want to make one thing clear – a merger with a SPAC is not the same thing as a trade sale. It is simply one of the pathways to becoming a public company, where the target management is pretty much left “holding the baby”, once the merger transaction between the SPAC and the target is completed.

That being said, I wanted to write Part 2 of the article, in order to give a few examples of transactions that might resonate with smaller high-growth Swiss companies, and to briefly talk about the latest trends in SPACs in the US and Europe.

I was previously making the case that a lot of SPACs tend to acquire significantly larger companies than the average Swiss start-up or scale-up, but that mergers with SPACs at the lower end of the scale are not implausible.

I have got some good news…

There are now some examples of recently proposed or completed transactions at the lower end of the scale (target enterprise value below USD 1bn) from the 2020 batch of US SPAC IPOs. While it may be a small number of cases (from what I can see, about 13% of the completed or proposed transactions involving the above-mentioned batch of SPACs), at least it is happening.

To illustrate some of the smaller deals, I thought it might be useful to mention a handful of transactions that might be interesting for various reasons:

· The exception to the rule: In most cases, SPACs acquire a single sizeable company. In this particular case, the SPAC (Greenrose Acquisition Corporation), acquired 4 companies simultaneously. The purpose: vertical integration and creation of a cash flow positive platform, in the cannabis market. In addition to the USD 172m raised at the IPO, the SPAC also raised USD 150m through a private placement consisting of a mixture of common stock and debt. More info here.

· Some of the smallest US SPACs listed in 2020 and their acquisition targets:

Newborn Acquisition Corp. raised USD 50m at IPO, to acquire an operating business domiciled in and around Asia (excluding China) and the United States. The SPAC acquired Nuvve Corporation, a vehicle-to-grid (V2G) technology company headquartered in the US, but with strong European connections. A further USD 18m was raised through a private placement (PIPE) and bridge financing. Assuming no debt outstanding, the combined company’s pro forma enterprise value was expected to be approximately USD 132 million. The current market cap of Nuvve Holding Corp, the post-merger entity, is approximately USD 190m. More info here.

LifeSci Acquisition Corp. raised USD 60m at IPO. On Sept 29, 2020 the SPAC announced a merger agreement with Vincera Pharma (clinical, oncology). No further capital (through a PIPE) seems to have been raised in this case. More info here. The current market cap of Vincerx Pharma Inc (new name post-merger) is approx. USD 280m and the share price evolution can be seen here.

Vistas Media Acquisition raised USD 100m at IPO, to identify a target business in the Global Media & Entertainment sector. With the help of a PIPE financing of USD 40m, Anghami, a Spotify rival headquartered in Abu-Dhabi, is set to become the first Arab technology company to list on NASDAQ New York via a merger with the Vistas SPAC. According to Anghami, the transaction implies an initial pro-forma enterprise valuation of approximately USD 220m, or 2.5x 2022 estimated revenues. More info here.

Although not always in the sub-USD 1bn enterprise value, you may also wish to have a look at:

· Some examples of transactions in the healthcare space (proposed):

Renovacor (preclinical, gene therapy) and Chardan Healthcare Acquisition 2. More info here.

Humacyte (clinical, tissue engineering) and Alpha Healthcare Acquisition. More info here.

DocGo (last-mile telehealth provider) and Motion Acquisition Corp. More info here.

· Some examples of transactions in the tech space (proposed):

Airspan Networks (5G network software/hardware) and New Beginnings Acquisition Corp. More info here.

Redwire (space technology) and Genesis Park Acquisition Corp. More info here.

(completed) AppHarvest (AgTech) and Novus Capital Corporation. More info here.

The Bitcoin enthusiasts may wish to have a look at the proposed transaction between Cipher Mining Technologies Inc. (Bitcoin miner) and Good Works Acquisition. More info here.

I have also got some not-so-good news…

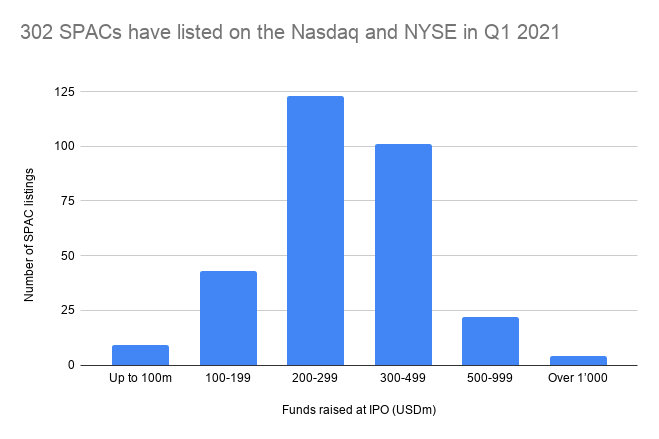

Firstly, the 2021 SPACs listed to date in the US are bigger than the ones listed in 2020. This means there are now more SPACs out there that will be looking for bigger targets. This makes a lot of them incompatible, at least for now, with the majority of Swiss start-ups and scale-ups.

Since the beginning of the year, there have been 302 new SPAC listings in the US. The table below shows that the largest growth has been in the USD 200-499m segment.

Secondly, according to Reuters, last week the US regulator opened an inquiry into the US SPAC frenzy1. This means from now on there will be an increased level of scrutiny on target due diligence, valuations, etc., which is of course not bad. However, the inquiry may also dampen the appetite of US investors for new SPACs, or for supporting existing SPACs through additional fundraising via PIPEs. The latter may in turn mean that SPACs would be looking for smaller targets than initially planned. Time will tell.

Thirdly, in Europe, the SPACs that are listing now are also quite big. It is my understanding that there is currently a lot of overlap between investors that invest in US SPACs and the ones that have invested in the recent European-listed ones. Therefore the investors’ expectations of a sizeable PIPE raising and of a target fair market value being at least 80% of the SPAC’s money in trust (although not imposed by the European exchanges) are likely to still influence the preference of SPACs for bigger deals, for a while.

Since my previous SPAC article, we have had two sizeable SPAC listings in Europe: ACQ Bure and EFIC1. Both of them happened last week.

ACQ Bure is Nasdaq Stockholm’s first SPAC IPO after the exchange changed the rules in early February 2021 to accommodate this type of vehicle. It raised the equivalent of CHF 380m to invest in “Nordic high-quality companies, with an enterprise value of approximately SEK 3-7 billion (CHF 750m) and which are operating in markets with great potential or in niche markets where the target company has a leading position.” Apparently, there are other SPACs in the pipeline that have a “more international flavour”2.

European FinTech IPO Company 1 (EFIC1), backed by a former co-head of UBS Global Wealth Management, listed on Euronext Amsterdam, and raised EUR 415m “to acquire a Financial Services or Financial Technology Company operating or headquartered in Europe, including the United Kingdom, or Israel”3.

Pegasus Europe, backed by the LVMH founder Bernard Arnault and former UniCredit chief Jean Pierre Mustier, is expected to be one of the next SPACs to list in Amsterdam, and is thought to be looking to raise “in the low hundreds of millions of euros” to invest in European financial companies4.

With regards to the smaller European SPACs, which would be much more relevant for a larger number of Swiss companies, my understanding from discussions with a number of European stock exchanges is that there are some “in preparation” for a listing. However, they are slower to come to the market because they would first like to see what the recently-listed larger SPACs are doing, how they are received by the market, how quickly they start announcing targets.

The good thing about European exchanges is that, as mentioned above, they do not impose a minimum acquisition size versus SPAC money in trust. This makes me think that, in the case of the future European-listed SPACs, we are likely to see more of them going for a multiple acquisition strategy of several smaller targets (similar to the Greenrose example). That is also more likely to happen once the European investors increase their interest in SPACs, which means less dependence on implementing the US model (of mainly one large acquisition) on a like-for-like basis.

To gain a better understanding of how a SPAC transaction works, from a target’s perspective, a Part 3 of this series is planned.

https://www.reuters.com/article/usa-sec-spacs-idUSL1N2LM3CH

https://www.bloomberg.com/news/articles/2021-03-16/first-spac-in-europe-s-rich-north-has-bankers-lining-up-for-more

https://efic1.com

https://www.ft.com/content/f523768d-41af-492c-95b0-ff5d23a30539