Letting capital flow to the global south

Letting capital flow to the global south

Channeling money from rich places to areas where it is needed has a positive impact. But how does that actually work? An introduction to the world of microfinance with Roland Dominicé from Symbiotics.

Entrepreneur in Cambodia in front of her new fish farm.

A woman in Cambodia shows us two water basins that were recently completed, a modest but quite lucrative fish farm built on her land. She financed the construction with a loan from a local microfinance bank. Her family owns two other assets that provide income: a big old truck that her husband drives to transport stuff and a rice polishing machine. Both were also financed with small loans and swiftly repaid. The specialized banks that provide small loans (worth a few hundred up to tens of thousands of euros) to people like her are collectively known as microfinance institutions (MFI).

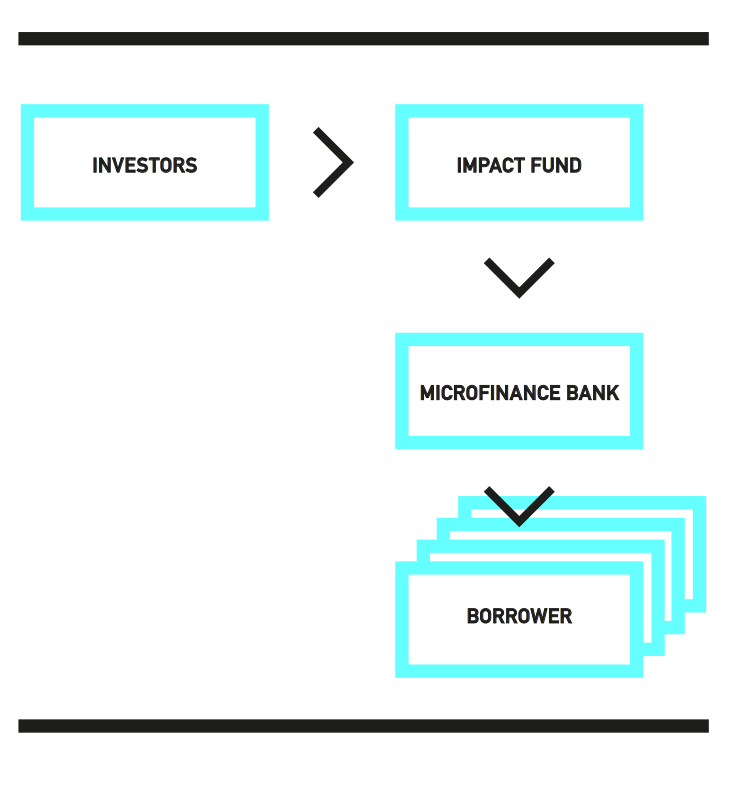

These banks also need to get their money from somewhere. Unlike banks in the western world, they can’t easily finance themselves with savings from the local population. So they have to turn elsewhere. This is where microfinance funds come in. These funds give loans to many different microfinance banks, maybe EUR 5 or 10 million at a time, and help the MFI grow and reach more people. The funds themselves get their money from institutional investors, such as pension funds, or from private investors. Microfinance funds have quite stable returns and report numbers related to the development impact they have: how many women they reach, how many of the borrowers live in a rural environment, etc.

How the money flows: Investors and impact funds are situated in the global North, while the microfinance banks and the borrowers are situated in the global South.

This branch of development finance was pioneered in late 1970 by Muhammad Yunus, who founded a “village bank,” Grameen Bank. He was later awarded a Nobel Peace Prize for his work. Since then, the idea has caught on, and the number of MFI has grown substantially. The number of funds that finance the MFI and other similar projects has grown to 435 in 2020, and the total assets they manage to USD 33 billion. Some of them specialize in topics such as energy or housing, and some also invest in equity, not just in loans. Collectively, they are called private asset impact funds—because their goal is to make an impact according to the Sustainable Development Goals (SDG). Switzerland is home to the biggest of these funds and accounts for 35% of the assets managed in this space.

In order to discuss the growing importance of impact funds and see where their journey will lead to, I talked to Roland Dominicé, the CEO and co-founder of Geneva-based Symbiotics, one of the three leading impact investing companies in Switzerland. In case you’ve never heard of Symbiotics, this is not surprising: The firm structures loans that will find their way into funds that are distributed by global banks. Since 2005, Symbiotics has done more than 4000 micro-finance deals, representing over USD 5.5 billion in loans. Symbiotics recently published the 2020 update of their yearly survey about impact funds.

Roland Dominicé, CEO and co-founder of Symbiotics.

How to reduce poverty

My first question to you, Roland: The first Sustainable Development Goal is to “End poverty in all its forms everywhere.” This is also the goal that most impact funds subscribe to, according to the survey. How can lending money reduce poverty?

Reducing poverty is the main claim of microfinance, and it has been shown to work in countless studies. Financial inclusion through access to loans brings financial security, increases consumption and investment, and creates jobs. The first point is to give people a means to overcome financial stress; for example, if a family member falls ill, without having to resort to loan sharks. The second point is to enable consumption that improves the situation of families; for example, by being able to buy a motorcycle or a fridge—things that we take for granted here. And thirdly, successful micro-entrepreneurs create jobs.

Facts from the survey: End-borrower outreach is tilted towards rural (59%) and women borrowers (69%), and the median loan balance is USD 1,800. The top five countries for investments are India (13%), Ecuador (5%), Cambodia (5%), Georgia (4%), and Mexico (4%). Impact funds mainly lend to lower-middle-income countries (gross national income [GNI] per capita between USD1,036 and USD 4,045) and upper-middle-income countries (GNI per capita between USD 4,046 and USD 12,535).

Q: Why don’t impact funds lend more to low-income countries?

A: The vast majority of emerging and frontier economies are in these two middle-income categories. The reasons why impact fund managers shy away from lending to banks in countries such as Chad, Sierra Leone, or Mozambique are political and economic. There is often corruption and instability, there are very high currency fluctuations, and the write-offs from bad loans are higher. It is also a question of size. These countries are much smaller than middle-income countries such as Mexico, Pakistan, or India. Often, the first funds to enter a low-income country are blended finance actors.

Brief explainer: How state actors expand the reach of microfinance

Blended finance means that state actors team up with private actors to address the problems Roland described above. It is a way to push private capital to places where it wouldn’t go otherwise. Central to blended finance are development finance institutions (DFI), which are owned and established by governments, such as the Deutsche Investitions- und Entwicklungsgesellschaft (DEG) or the Swiss Investment Fund for Emerging Markets (SIFEM).

Blended finance: Loans are structured so that public actors bear the first losses, which entices private investors to invest.

The mechanism behind blended finance is simple: In a blended fund, the first losses from microfinance banks that don’t pay back their loans are borne by the development finance institutions. This offers private investors a level of protection that makes them feel comfortable enough to invest.

Q: This is a nice setup, Roland. Are losses reserved for the taxpayers and the profits for private investors?

A: The idea behind blended finance is to push money to places it wouldn’t flow otherwise. It allows financial institutions in very poor countries to grow and establish a track record. If it works, public money isn’t needed anymore in the future. We did a carefully designed fund for UBS, for example. They didn’t have a private debt impact fund before. The Swiss Development Finance Institution SIFEM allocated CHF 2.5 million to this fund, which allowed the fund to raise CHF 50 million in the end. In the field of blended finance, this multiplier effect, 25 times in this case, is the definition of success.

Until now, we’ve talked about the classic model of microfinance (funds -> microfinance banks -> borrowers). This is still the biggest part of what impact funds do (around 85% of total volume). But there are new, different forms emerging, namely, equity investments and loans that go directly to small and medium-sized enterprises (SMEs) or projects in specific sectors such as renewable energy. As Roland explained to me, the reason why the classic model is here to stay is that for a foreign fund, it is more efficient to go through an aggregator of loans (i.e., a microfinance bank), than investing directly into a company or a project. In case of such a direct loan to a company (fund -> SME, without a microfinance bank in between), the investment sizes are usually USD 1 million or more—so we’re talking about rather large companies here, not a food kiosk on some corner. When it comes to equity investing, the typical case is a fund purchasing a minority stake in a microfinance institution they already work with. It is quite a safe bet because these banks are well diversified, so this kind of equity play has attractive returns and moderate risks.

Where does the money ultimately come from?

According to the Symbiotics survey, the impact funds receive 52% of their funding from institutional investors, followed by 27% from private retail and qualified individuals, and the rest (21%) from public funders. Impact investing strategies brought positive financial returns for investors in 2019, with net returns above the 4% mark (in USD).

As Roland tells me, it is no surprise that pension funds, life insurance companies, and similar investors like this type of funds. Impact investments are inherently illiquid, which means that you need to be invested for years to come. But these institutional investors also have long-term liabilities, so the time frames nicely match.

Many private banking clients would surely also like to invest, Roland adds, because of the impact angle. But there aren’t many products that are available for retail investors. ( responsAbility Global Micro and SME Finance Fund are two.) There are initiatives to change this, though. “A lot of stuff is happening behind the scenes, and hopefully more private banking clients will get access to microfinance soon,” he adds.

How can investors actually be sure that “impact” isn’t just a clever marketing ploy?

As Roland explains, the impact these investments have is measured and reported on three different levels.

Environmental, social and governance (ESG) ratings: Almost all funds report the ESG ratings of the institutions they invest in. These are numbers about environmental impact, social concerns such as diversity and borrower protection (which is important in this field to prevent over-indebtedness), and the governance of these institutions.

SDG intent: Most funds report on what impact their investments have in furthering the sustainable development goals. We heard about SDG 1 (reducing poverty), which is the primary goal. SGD 5, (gender equality), and SDG 8, (decent work and economic growth), are also often targeted and reported.

Financial inclusion: This reporting layer measures how good a microfinance bank is at reaching out to people who are excluded from the financial world, e.g., those living in remote rural areas. A bank that concentrates on people living in the cities might be more profitable but would have a lesser score on the inclusion target.

Symbiotics’ survey shows that impact funds have come a long way and that they offer a way to make money and have a positive impact at the same time. For many small entrepreneurs, getting access to capital has the potential to change their lives and be the first step out of poverty.